U.S. Broiler and Turkey Exports, January-February 2024

OVERVIEW

Total exports of bone-in broiler parts and feet during January-February 2024 attained 573,029 metric tons, 7.2 percent lower than in January-February 2023 (617,370 metric tons). Total value of broiler exports increased by 0.7 percent to $751.8 million ($746.5 million).

Total exports of bone-in broiler parts and feet during January-February 2024 attained 573,029 metric tons, 7.2 percent lower than in January-February 2023 (617,370 metric tons). Total value of broiler exports increased by 0.7 percent to $751.8 million ($746.5 million).

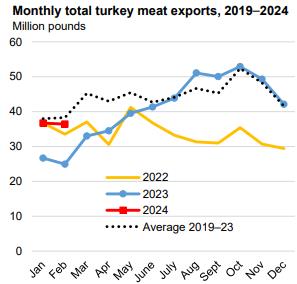

Total export volume of turkey products during January-February 2024 attained 33,173 metric tons, 41.7 percent more than in January-February 2023 (23,404 metric tons). Total value of turkey exports increased by 12.7 percent to $90.5 million ($80.3 million).

Unit price for the broiler industry is constrained by the fact that leg quarters comprise over 97 percent of broiler meat exports by volume (excluding feet). From the first quarter of 2021 through 2022, unit value of leg quarters increased consistent with international demand followed by a decline in 2023. Leg quarters represent a relatively low-value undifferentiated commodity lacking in pricing power. Exporters of commodities are subjected to competition from domestic production in importing nations. Generic products such as leg quarters are vulnerable to trade disputes and embargos based on real or contrived disease restrictions.

HPAI has emerged as a panornitic affecting the poultry meat industries of four continents with seasonal outbreaks. The distribution in the U.S. limits eligibility for export depending on restrictions imposed by importing nations

Ongoing outbreaks of African swine fever in China and Southeast Asia from early 2019 and Europe from 2010 onwards reduced the availability of pork. In addition, disruptions in chicken production and logistics due to COVID restrictions decreased availability of protein with international repercussions on trade in chicken and pork. The demand for pork imports to China has diminished with restoration of domestic hog production. Mild overproduction is evident in the white-feathered broiler sector with implications for exports other than feet extending into 2024.

EXPORT VOLUMES AND PRICES FOR BROILER MEAT

During January-February 2024 the National Chicken Council (NCC), citing USDA-FAS data, documented exports of 578,170 metric tons of chicken parts and other forms (whole and prepared), down 6.9 percent from January-February 2023. Exports were valued at $395.0 million with a weighted average unit value of $1,301 per metric ton.

During January-February 2024 the National Chicken Council (NCC), citing USDA-FAS data, documented exports of 578,170 metric tons of chicken parts and other forms (whole and prepared), down 6.9 percent from January-February 2023. Exports were valued at $395.0 million with a weighted average unit value of $1,301 per metric ton.

The NCC breakdown of chicken exports for January 2024 by proportion and unit price for each category compared with the corresponding month in 2023 (with the unit price in parentheses) comprised:-

- Chicken parts (excluding feet) 2%; Unit value $1,256 per metric ton ($1,164)

- Prepared chicken 2%; Unit value $4,501 per metric ton ($4,202)

- Whole chicken 6%; Unit value $1,789 per metric ton ($1,593)

- Composite Total 0%; Av. value $1,330 per metric ton ($1,222)

The following table prepared from USDA data circulated by the USAPEEC, compares values for poultry meat exports during January-February 2024 compared with the corresponding months of 2023:-

|

PRODUCT

|

Jan.-Feb. 2023

|

Jan.-Feb. 2024

|

DIFFERENCE

|

|

Broiler Meat & Feet

|

|

|

|

|

Volume (metric tons)

|

617,370

|

573,029

|

-4,432 (-7.2%)

|

|

Value ($ millions)

|

746.5

|

751.8

|

+5.3 (+0.7%)

|

|

Unit value ($/m. ton)

|

1,209

|

1,312

|

+103 (+8.5%)

|

|

Turkey Meat

|

|

|

|

|

Volume (metric tons)

|

23,404

|

33,172

|

+9,768 (+41.7%)

|

|

Value ($ millions)

|

11.2

|

12.2

|

+1.0 ( +8.9%)

|

|

Unit value ($/m. ton)

|

4,786

|

3,678

|

-1,108 (-23.2%)

|

COMPARISON OF U.S. CHICKEN AND TURKEY EXPORTS

JANUARY-FEBRUATY 2024 COMPARED TO 2023

BROILER EXPORTS

Total broiler parts, predominantly leg quarters but including feet, exported during January-February 2024 compared with January-February 2023 declined by 7.2 percent in volume but was up 0.7 percent in value. Unit value was 8.5 percent higher to $1,312 per metric ton.

Total broiler parts, predominantly leg quarters but including feet, exported during January-February 2024 compared with January-February 2023 declined by 7.2 percent in volume but was up 0.7 percent in value. Unit value was 8.5 percent higher to $1,312 per metric ton.

During 2023 exports attained 3,635,178 metric tons valued at $4,739 million, down 4.2 percent in volume and down 9.2 percent in value compared to 2022. Unit value was down 9.5 percent to $1,284 per metric ton

Broiler imports in 2023 were projected to attain 72,000 metric tons (158 million lbs.)

The top five importers of broiler meat represented 49.5 percent of shipments during January 2024. The top ten importers comprised 66.9 percent of the total volume reflecting concentration among the significant importing nations.

During January-February 2024 Mexico was the first-ranked importer by volume and value with 124,385 metric tons representing 21.7 percent of export volume up 2.1 percent from January-February 2023. Value at $146.1 million was 19.5 percent of the total for exported broiler products during January-February 2024 and up 17.9 percent from 2023, but with a 16.6 percent increase in unit price to $1,179 per metric ton. Value was up 17.9 percent to $146.7 million with a 12.5 percent increase in unit price to $1,212 per metric ton. During February 2024 volume was up 2.2 percent to 61,325 metric tons and value increased15.0 percent from February 2023 to $74.3 million.

Taiwan was 2nd ranked as an importer during January-February 2024 with 47,439 metric tons valued at $146.7 million up 23.3 percent and 21.4 percent in volume and value respectively, compared to the previous year. Unit price was $1,236 per metric ton.

Cuba was the 3rd largest importer based on volume during January-February 2024 with 46,687 metric tons valued at $53.6 million down 10.5 percent in volume but up 5.9 percent in value compared to January-February 2023. Unit price was $1,146 per metric ton.

During January-February 2024 exports to China, 4th-ranked by volume and 2nd ranked by value represented 7.2 percent by volume and 18.1 percent by value of shipments. Exports were down 47.4 percent in volume to 41,272 metric tons and down 56.4 percent in value to $81.4 million compared to January-February 2023. Unit price was $1,972 per metric ton up 21.5 percent.

For 2023, 405,313 metric tons of U.S. broiler products were shipped to China, valued at $711,172 with an average unit value of $1,755 per metric ton. A breakdown of product categories and prices was provided by USAPEEC. Paws and feet represented 68.5 percent of volume and 73.1 percent of value with a unit price of $1,871 per metric ton. Legs and leg quarters comprising 22.6 percent of volume and 12.8 percent of value were priced at $990 per metric ton below the $1,302 average for all U.S. exports excluding China. Wings comprised 4.6 percent of volume and 5.7 percent of value with a unit price of $2,190 per metric ton. All other poultry products (including 4 tons of duck meat) amounting to 4.2 percent of volume and 8.4 percent of value attained an average unit price of $3,485 per metric ton

During January-February 2023 exports to Hong Kong increased by 222 percent in volume to 14,300 metric tons and 171 percent in value to $21.5 million with a unit price of $1,504 per metric ton. In 2022 and 2023 unit prices were $1,834 and $1,671 per metric ton respectively. Accordingly consignments are presumed to comprise a high proportion of feet with assumed transshipment to the Mainland as in past years.

During January-February 2024 nations gaining in volume compared to the corresponding period in 2022 (with the percentage change indicated) in descending order of volume with ranking indicated by numeral were:-

- Mexico (+1%); 2.Taiwan, (+23%); 5, Guatemala, (+3%); 6. Philippines, (+53%); 7. UAE, (+77%); 9. Viet Nam, (+18%) and 11. Hong-Kong, (+222%).

Losses during January-February 2024 offset the gains in exports with declines for:-

- Cuba, (-10.0%); 4. China, (-47%); 8. Canada, (-4%); 10.Angola, (-23%) 13. Haiti, (-31%).

TURKEY EXPORTS

The volume of turkey meat exported during January-February 2024 increased by 41.7 percent to 33,172 metric tons from January-February 2023 and value was 18.9 percent higher to $121.2 million compared to January-February 2023. Average unit value was 23.2 percent lower to $3,678 per metric ton.

Imports of turkey products were projected to rise to 38,640 metric tons in 2023.

For the entire year of 2023 export volume increased by 20.2 percent to 221,098 metric tons compared to 2022 and value fell by 2.0 percent to $620 million reflecting an 18.5 percent decrease in unit value to $2,829 per metric ton.

Mexico was the leading importer of turkey products during January- February 2024 with 24,120 metric tons representing 72.7 percent of total volume of 35,172 metric tons. Value at 64.6 million was 71.4 percent of the total with a unit price of $2,678 per metric ton. Volume was 44.4 percent higher and value was 9.3 percent higher than for January-February 2023.

The regions of the Caribbean (2,722 metric tons); East Asia, (998); Central America, (1,260) and sub-Saharan Africa (1,612) collectively imported 6,592 metric tons of turkey products in January-February 2024 representing 19.9 percent of volume and 20.7 percent of value amounting to $18.7 million. Unit price was $2,536. Regional unit prices per metric ton ranged from $1,652 for the Leeward-Windward Islands to $3,189 for Canada.

During January-February 2024 nations increasing volumes of purchases, albeit over a small base, compared to the corresponding months in 2023 with ranking comprised:-

- Mexico, (+44%); Leeward-Windward Islands, (+45%); Dominican Republic, (+317%) and South Africa, (1,618%)

- Canada reduced imports by 5 percent and 4. Jamaica by 51%).

PROSPECTS FOR 2024

The April 17th 2024 Livestock, Dairy and Poultry Outlook Report, retained the projection for 2023 exports of broiler products at 3.302 million metric tons (7,265 million lbs.). This value represents 15.7 percent of the projected production of 21.083 million metric tons (46,387 million lb.) of broiler RTC by the U.S. industry.

For 2024 exports of broiler products were forecast at 3.209 million metric tons (7,060 million lbs.), equivalent to 14.9 percent of forecast annual production of 21.409 million metric tons (46,875 million lbs.)

Projected export of turkey products in 2023 will be 222,272 metric tons, (489 million lbs.) or 9.0 percent of annual production of 2.481 million metric tons (5,457 million lbs.).

For 2024 exports of turkey products were forecast at 236,400 metric tons (520 million lbs.) equivalent to 9.7 percent of forecast annual production of 2.441 million metric tons (5,375 million lbs.)

It is important to recognize that exports of chicken and turkey meat products to our USMCA partners amounted to $1,264 million in 2021, $1,647 million during 2022 and $1,696 in 2023. It will be necessary for all three parties to the USMCA to respect the terms of the agreement since punitive action against Mexico or Canada on issues unrelated to poultry products will result in reciprocal action by our trading partners to the possible detriment of U.S. agro-industries.

The emergence of H5N1strain avian influenza virus with a Eurasian genome in migratory waterfowl in all four Flyways during 2022 was responsible for sporadic outbreaks of avian influenza in backyard flocks and serious commercial losses in egg-producing complexes and turkey flocks but to a lesser extent in broilers. The probability of outbreaks of HPAI over succeeding weeks appears more likely as spring migration of waterfowl has commenced. Incident cases during April resulted in depletion of 8.5 million hens and a turkey flock. Outbreaks will be a function of shedding by migratory and domestic birds and possibly mammals. The extent of protection of commercial flocks at present relies on the intensity and efficiency of biosecurity, representing investment in structural improvements and operational procedures. These measures are apparently inadequate to provide absolute protection, suggesting the need for preventive vaccination in high-risk areas for egg-producing, breeder and turkey flocks.

The application of restricted county-wide embargos following the limited and regional cases of HPAI in broilers with restoration of eligibility 28 days after decontamination has supported export volume for the U.S. broiler industry. Exports of turkey products were more constrained with plants processing turkeys in Minnesota, the Dakotas, Wisconsin and Iowa impacted. Most nations have now lifted embargos that were previously placed on entire states or counties following outbreaks in the 4th quarter of 2024 as the WOAH mandated post-decontamination period has expired. The challenge will be to gain acceptance for vaccination based on intensive surveillance. Recognition that H5N1 HPAI is panornitic in distribution across six continents and is now seasonally or regionally endemic in many nations with intensive poultry production, suggests that vaccination will have to be accepted among trading partners as an adjunct to control measures in accordance with WOAH policy.

The live-bird market system supplying metropolitan areas, the presence of numerous backyard flocks, fighting cocks and commercial laying hens allowed outside access, potentially in contact with migratory and now some resident bird species, all represent an ongoing danger to the entire U.S. commercial industry. The live-bird segments of U.S. poultry production represent a risk to the export eligibility of the broiler and turkey industries notwithstanding compartmentalization for breeders and regionalization to counties or states for commercial production.